Missed the Reassessment Window? Here’s What You Can Still Do

Missed the Reassessment Window? Here’s What You Can Still Do

Welcome back, friends! This post is part two of a 12-part series we recently launched called The Loan Officer’s Guide to Appraisals. In case you missed part one, go back and read all about the Final Inspection process here. In this blog post, we’re going to give you an appraiser’s perspective on unique homes, and help you get the tools you need to successfully navigate lending on those sometimes quirky, atypical, and hard to… well, everything, homes!

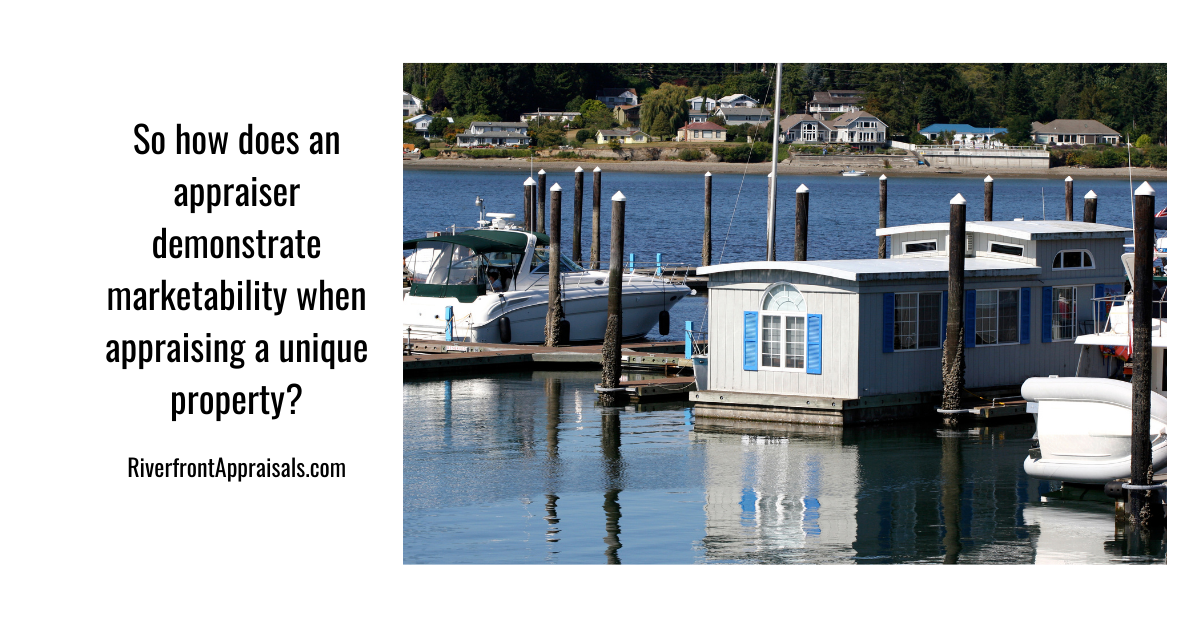

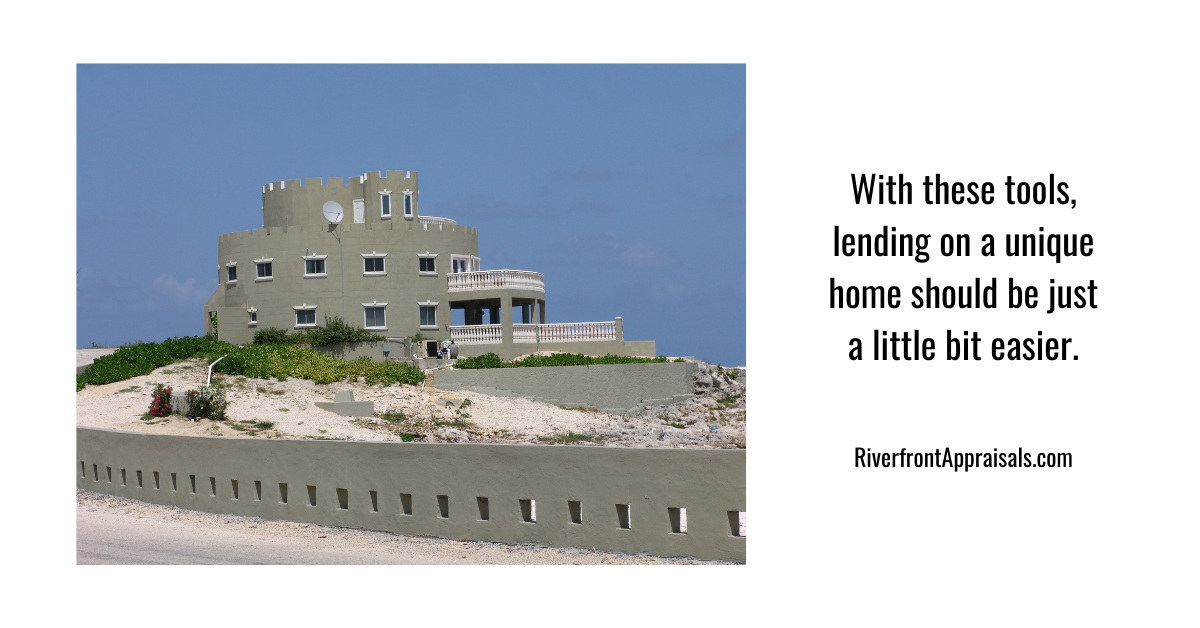

I work in the western Kentucky and southwestern Indiana areas, where we have an abundance of agricultural properties. So homes with 20, 50, or 100+ acres are common. Manufactured homes are common here, but not in other parts of the country. And every once in a while we’ll see a log home, earth berm home, or silo home. Other parts of the country see barndominiums, churches converted to residences, geodesic A-frame homes, houseboats, castles, or you name it – the list goes on.

When you lend on a three bedroom, two bath Ranch-style home with 1,500 square feet of living space, and the home is in a neighborhood with 20 sales of similar homes in the last year, it’s a slam dunk! Easy for you, easy for the appraiser. All the appraiser has to do is find a minimum of three homes similar to the subject, which won’t be hard at all!

Why is this such a concern? From a lender’s perspective, you are concerned with many things, of course – not the least of which is marketability. The lender wants to know how difficult it would be to sell the home if the borrower defaults on their mortgage.

So how does an appraiser demonstrate marketability when appraising a unique property?

The best way for an appraiser to demonstrate marketability of any home is by analyzing closed sales of similar properties. For example, If I’m appraising a double wide manufactured home on 20 acres, then if I have a sale of a similar manufactured home on say, 15-25 acres, then that should suffice.

But what does an appraiser do when there are no recent sales? I’m going to share with you five things an appraiser can do to help you make a lending decision on that out of the ordinary property. One thing to keep in mind as a lender, is that when lending on unique properties, it’s helpful to think outside the box. It’s helpful for the lender, and definitely helpful for the appraiser.

Dated Sales

If the appraiser is having a hard time finding recent sales, one thing that can be done is to look for sales which sold in the past five years or so. Obviously, the more recent sale the better, but perhaps my research revealed a model match of a unique home that sold four years ago. Am I going to use it? Absolutely! I may need to account for changes in the market (positive or negative market conditions), but other than that, sometimes a dated sale is very helpful.

[bctt tweet=”Why is this such a concern? From a lender’s perspective, you are concerned with many things, of course – not the least of which is marketability. The lender wants to know how difficult it would be to sell the home if the borrower defaults on their mortgage.” username=”RiverfrontApp”]

Active or Pending Listings

We can learn a lot from the market if we analyze not just sales, but active or pending listings. While an active listing doesn’t carry as much weight as a closed sale, it can provide some insight into the market, or a specific style of home. Maybe I’m appraising a condo unit in a development that sees very few sales. Ever. However, there just happens to be a unit for sale. In this case, I should consider including this listing in the appraisal. List price, days on market, similar amenities, etc can all be used to support an appraiser’s opinion of value, even coming from an active listing.

Sales of Other Atypical Properties

Lending on a log home? If a log home is atypical for your market, then why not consider sales of other atypical homes? An appraiser will definitely be considering sales of homes that may be outside the norm when appraising a unique property. So if I’m appraising a log home in a market with few similar sales, I’ll also be searching for sales of nicer manufactured homes, earth berm homes, barn homes, or other unique properties. This – together with adequate analysis and explanation – can go a long way to proving marketability and supporting a value.

Sales in Other Markets

My hometown is on the Ohio River. Properties along the river usually sell for a mint. The hard thing is that they hardly ever sell. Occasionally, I’ll look to our neighbors down the river and across the river for sales, to support my opinion of value, or to support my opinion that a river view is beneficial and commands a premium. I have to keep in mind to make any necessary adjustment for location differences between the two communities, but it can definitely be done, and can certainly be helpful.

Sales Which Bracket ‘That One’ Feature

Most underwriters like to see all the features of a home ‘bracketed’. For example, if the home has 2,500 square feet of GLA, they want to see comps with more and with less than 2,500 square feet. If the home has a three-car garage, four bedrooms, and is situated on five acres, they want to see sales with similar amenities. This isn’t always easy. Often in rural markets, I explain to homeowners that the sales in the appraisal might not all be completely identical to their home. Sometimes I may need to include a sale only for the purpose of bracketing one feature of the subject. Maybe my subject is an old 800 square foot farmhouse in the county. I have plenty of sales of older homes, but in order to find a small home like that, I have to include a sale in the city. Or perhaps I have a sale in the city that happens to have a large pole barn. I might need to go out 10 miles to the rural neighborhoods to find a sale of a home with a large barn. This is entirely acceptable, and often necessary, as long as the appraiser explains why they did what they did, and if it results in any affect on value or marketability.

Lending on unique homes can either be a pain or a pleasure. One way to ensure you make the most of lending on a unique home, is understanding how an appraiser can and should approach the appraisal assignment. With these tools, lending on a unique home should be just a little bit easier.

If you have any other specific questions about lending on unique homes, and how the appraiser can help you and your client get to the closing table quicker and easier, send us an email to info@theappraisalcast.com.

Committed to helping you understand your home’s market value,

Ryan Bays, SRA, AI-RRS

Missed the Reassessment Window? Here’s What You Can Still Do

It’s reassessment season for most folks in our area. Homeowners

I feel like we all need a laugh. How about